06/03/2023

Inflation and the impact on insurance and claims

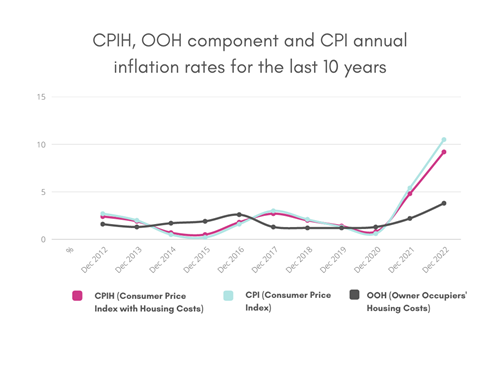

Inflation has an impact on all of us, every day. But over the past year, its influence has been particularly noticeable. After years of low inflation, it rose sharply in 2022 as the cost of food, fuel, goods and services increased significantly.

Unfortunately, insurance has not been immune to this.

Why is inflation high?

A number of economic and political events have pushed up inflation.

The cost of energy has been particularly influential. The demand for energy sources such as gas and oil have risen after the pandemic, causing prices to rise.

This situation was then made worse by the start of the war in Ukraine. This limited the supply of energy from Russia, which again caused prices to soar.

Food prices have also risen, which has contributed towards the escalating rate of inflation. This is again linked to the war in Ukraine, as the country was a major supply of grain.

In addition, Ukraine is also a huge producer of neon gas. This production has been disrupted, which has had a knock-on effect on the manufacture of microchips, which are used in many of our technological products.

Shortages and price increases for parts needed to repair vehicles are contributing too.

(Source: Office for National Statistics - Consumer Price Inflation)

How does high inflation impact insurance?

A high rate of inflation affects insurance in several ways.

- Claims inflation

Claims costs have increased because of the higher cost of materials and wage inflation. This means that if you make a claim, the insurer will have to pay more to compensate you or a third party.

For instance, if your car is involved in an incident, it will cost the insurer more to replace or repair it.

- Underinsurance

As inflation increases the value of assets and property, it also increases the risk of your assets or home being underinsured.

This is because your sum insured may now be too low.

For instance, perhaps you estimated that the rebuild cost of your home was £200,000. However, thanks to inflation, the actual rebuild cost of your home is now £250,000.

If the worst happens, and your home is completely destroyed, your Home Insurance will only pay out the maximum sum of £200,000. This means you would need to find an additional £50,000 to complete the build.

To combat this, we recommend getting regular professional valuations. Preferably, this should be done by an RICS-qualified surveyor. If you’re at all unsure about your rebuild value, speak to us to get extra guidance.

- Insufficient Business Interruption cover

Business Interruption cover should also be carefully reviewed.

Lead times to rebuild or replace lost property could now be much longer than anticipated. This means your indemnity period (the period of cover during which your business should recover to pre-loss levels of trading), could be too short.

Due to inflation, it may also cost a lot more to replace or rebuild your property. Your indemnity limit should therefore be reviewed too.

- Increased premiums

Sadly, it is inevitable that price rises will also result in insurance premiums going up as insurers seek to manage their own costs. To help you keep your premiums down, speak to us well before your renewal date. We can then work with you to find the right insurance for the right price.

We can also provide risk management services for businesses, which may help to trim your costs.

Speak to us about your insurance needs

If you’d like to talk about your renewal or get a quote, speak to our experienced brokers today. Our friendly and approachable team will get to know you and your needs to find the right policy.

Find out more about Business Insurance or Personal Insurance.

Related Articles